I Applied For 13 Credit Cards Last Year. Here’s What Happened To My Credit Score

I’ve always enjoyed playing the credit card rewards game and earning points to use for free cash back, groceries, and travel. Last year I upped the ante with the goal of earning enough travel and hotel points to pay for our trip to Scotland and Ireland this summer. To level up my rewards I had to apply for new cards – 13 of them to be exact. The end result was an assault on my credit score that would make any personal finance blogger bury their head in shame.

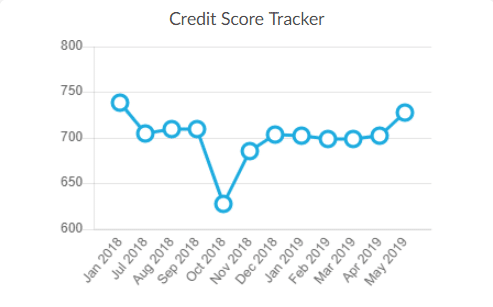

Yes, in the process of earning more than 1 million rewards points my credit score sunk to new depths – dropping 122 points in less than a year.

What happened to my credit score?

I’ve never had an impeccable credit score like some people who boast scores over 800. I’ve been dabbling in credit card rewards for several years and all the new inquiries and age of accounts tend to drag down my score. Still, I started 2018 with a solid credit score of 749 – enough to receive an “Excellent” grade from the good folks at Equifax.

Early in the year I applied for the

Next up was the

Finally, I applied for the PC Financial World Elite MasterCard to take advantage of the no-fee card and bonus PC Points on shopping at Loblaws stores, Shoppers Drug Mart, and Esso gas stations.

No Credit Checks from Amex or TD

I should point out that during this time I had also applied for the American Express Platinum Card, as well as the Marriott Bonvoy American Express Card and the Marriott Bonvoy Business American Express Card. As a current and long-time American Express cardholder I did not have a credit check pulled with those applications.

I also applied for the

Application denied

What I didn’t discover until later in the year was that all of these inquiries took a toll on my credit score – dropping it by 40 points or so by the middle of July.

In the meantime, I was on a roll and applied for another BMO card – this time the World Elite MasterCard. In hindsight I should have done a product switch from the BMO World Elite Air Miles Card to the World Elite Card, but I had cancelled the Air Miles credit card shortly after receiving the bonus. Damn – didn’t need that extra credit hit!

Related: Why is cancelling a credit card so hard?

Then my first rejection – I applied for the HSBC World Elite MasterCard, which came with an awesome sign-up bonus and first year free. Denied! I also applied for a BMO business credit card. Denied again!

It’s at this time that I login to my Borrowell* account and check out what happened to my credit score. I also wanted to see if there’s anything odd in my credit report. Sure enough, I discovered multiple credit hits from CIBC after my Aventura misadventure from the summer. There’s two extra credit hits I didn’t need.

*Note: If you haven’t checked out your free credit score and report with Borrowell you should do so now. They also just released a super convenient mobile app that allows you to monitor your credit score and credit reporting information in real time.

By October 2018 my credit score had plummeted to 627 – a “below average” score according to Equifax. While a low credit score is not exactly devastating to someone who technically doesn’t need credit – I just like to collect rewards points – this poor score would clearly prevent me from getting approved for new applications.

Road to Recovery

After that discovery I put a hold on any new credit card applications. I had already earned enough points for our trip to Scotland and Ireland, so there was no point being greedy. It was time to repair my credit score.

It didn’t take long. After all, I pay my bills on time and pay off my credit cards in full each month. The 122 point drop in my credit score matches up with a common belief that each new credit inquiry lowers your credit score (temporarily) by 10 points. The extra credit hits from CIBC didn’t help, and so by October my score had suffered from all of these new inquiries within a short time-frame.

By November my credit score had jumped 50 points and then by December it had climbed back over 700. There it hovered for several months before jumping again in May to around 730.

The increased credit score doesn’t mean much – again, I’m not applying for a mortgage, car loan, or line of credit. But I’m grateful that my score is once again closing in on “Excellent” in the eyes of lenders. That’s because there are some very tempting credit card offers on the market right now and it’s time for me to get back into the rewards game!

I too thought that Amex didn’t do credit checks because I didn’t see any hits on my Equifax record. However, I then checked my Transunion profile and saw all the enquiries they made over the years.

Equifax should be shut down. This company is ruining people’s lives

What I don’t understand is that since you’ve been playing with credit cards reward games for some years, don’t you already have most of the cards?

Or maybe you cancelled them and reapplied them. Sorry I’m new to all this.

Hi Illa, the idea is to sign-up for new cards to take advantage of the welcome bonuses and then cancel them within a year before the annual fee comes due. So, yes, I’ve reapplied for several of the same cards over the years.

Another trick that I’ve more recently learned is instead of cancelling a card, you can ask for a “product switch” to move to another rewards card within the same family. This keeps your account open (i.e. no new credit check) and can get you access to a bonus from a new card.

Two examples of successful product switches:

1. TD Aeroplan Visa Infinite to TD First Class Travel Visa Infinite (or vice-versa)

2. RBC Avion Visa Infinite to RBC WestJet World Elite MasterCard (or vice-versa)

[…] Over on Rewards Cards Canada I revealed that I applied for 13 credit cards last year. Here’s what happened to my credit score. […]

[…] from Boomer and Echo applied for 13 credit cards in 2018, this is what happened to his credit score. It was pretty crazy, he applied for so many he ended up getting denied an Amex card. […]

[…] Robb is a bit of an expert on this too. The whole reason you’re reading this article is because he travel hacked his way to Europe. […]